Stability breeds Instability and Warning always occur before Instability....

O Ashuji....One of the greatest work (not that I have read many) in study of volatility and price behavior has been done by Benoit Mandelbrot. His book "The (Mis) Behavior of Markets - A Fractal View of Risk, Ruin and Reward" is a must read for anyone who wants understand nature of price behavior in asset markets. Second last chapter in the book discusses - The Heresies of Finance. The one I found most powerful is -- Forecasting Prices May Be Perilious, but You Can Estimate the Odds of Future Volatility. I will quote from the book...

" The data overwhelmingly show that the magnitude of price changes depends on those of the past, and that the bell curve is a non-sense. Speaking Mathematically, markets can exhibit dependence without correlation. The key to this paradox lies in the distinction between the size and the direction of price changes. Suppose that the direction is uncorrelated with the past : The fact that prices fell yesterday does not make them more likely to fall today. It remains possible for the absolute changes to be dependent : A 10% fall yesterday may well increase the odds of another 10% move today - but provide no advance way of telling whether it will be up or down. If so, the correlation vanishes, in spite of the strong dependence. Large price changes tend to be followed by more large changes, positive or negative. Small changes tend to be followed by more small changes. VOLATILITY CLUSTERS."

For More on Concept of Clustering....

http://www.speculationanart.blogspot.in/2012/12/market-compression-reaches-extreme.html (Dated 26th December 2012)

25 Feb 2013.....Beginning of Volatility Clustering....!!!

I have discussed many times in past blog that 2012 was the most compressed year for Indian stock markets and many other global markets. Volatility was killed globally by various central bank interventions. In a sense it was clustering of compression. Something which has been calm for long, sudden surge indicates change in behavior. Rupee could be used here as an classic example. Rupee was largely stable between 44-47 (2010 till Aug 2011) for almost 18-19 months. Then between Aug-Sep 2011 it rose from 44 to 49. Basically 19 months range was broken in 2 months. This indicated big change coming. Anyone glued on fundamental would fail to understand or understand this move in hindsight but study of price behavior showed this market had changed. It indeed had and Rupee depreciated sharply between Aug-Dec 2011 and what has happened since then is known. Basically, any historically large move should be paid particular attention.

FUNDAMENTAL UNDERSTANDING CREATES ILLUSION OF CONTROL WHILE PRICE UNDERSTANDING WARNS OF CHANGING BEHAVIOR.

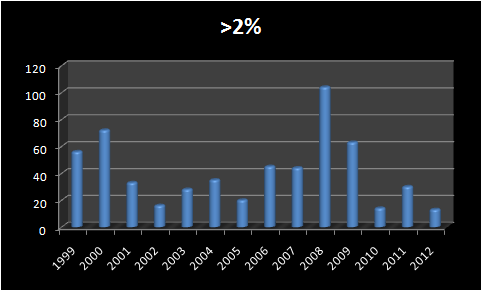

US VIX Spiked 32% on 25th Feb 2013. Since 2004, there have been 11 instances of 30+% VIX spike.

Since 1990, only 8 times VIX has spiked more than 35%

Analyzing above spikes within context of volatility clustering

Methodology used - Each spikes were analyzed with respect to VIX 2 months prior and 2 months post occurrence of spike i.e Feb 2007 was analzyed with respect to how VIX behaved 2 months prior to Feb 2007 and 2 months post Feb 2007.

1) 27 Feb 2007 VIX spikes 64.3% (highest ever in the history of VIX so far) - VIX range 2 months prior to spike (Jan-Feb 2007) was 10-12. Thus breaking that range or range of even longer prior period with such sharp spike should have warned of volatility. Volatility typically clusters and then subsides. This spike was followed by sharp moves in VIX both on downsides and upsides. But size of moves had certainly changed. within next 11 trading days, VIX had 5 double digit % moves (3 up and 2 down). SO WHAT CHANGED WITH THAT 64% SPIKE MOVE IN VIX....10-12 range became thing of past....12 became base and VIX gradually moved up all through 2007.

2) 29 Sep 2008 and 22 Oct 2008 clustering was right at the middle of Financial Crises.

3) 27 April 2010 sudden spike in VIX was prelude to 6th May 2010 Flash Crash and VIX peaking on same day with VIX falling by 30% on 10th May 2010.

4) 4th, 8th and 18th August 2011 clustering is clearly evident...it then got coupled with EU crises which culminated in last spike of 30+% on 9th Nov 2011.

Conclusion

1) Whenever such historic spike occurred, Volatility clustered. Except for May 2006, wherein VIX level came back to pre-spike level after a month or so, all other instances pre-spike level didn't come for very long time. Pre-Spike became base for VIX. Any Sharp fall in VIX towards pre-spike level immediately resulted in spike in VIX.

2) Volatility clustered and then subsided with VIX at higher levels.

3) 25 Feb 2013, VIX spiked from 14odd to 18.9...If history is any guide and nature of Volatility any VIX move towards 14 should result in spike in VIX towards 19 or higher at least in foreseeable future...

{kind=link}